Strategic location, strong economic growth and demographics dominated by the younger generation have made the Southeast Asian region a target for foreign investors.

The International Monetary Fund (IMF) in its October 2023 report estimates global economic growth of 3.5% in 2022, 3% in 2023, and 2.9% for 2024.

Meanwhile, the Asian Development Bank (ADB) estimates that the Southeast Asian economy will grow 4.6% in 2023 and 5.0% in 2024.

With high growth projections, Southeast Asia is considered a promising region for investment.

Foreign Direct Investment (FDI) or foreign direct investment funds towards Southeast Asian countries or those included in the Association of Southeast Asian Nations (ASEAN) group has relatively increased every year.

Referring to Aseanstats.org, total FDI to ASEAN in 2022 was recorded at US$ 224.2 billion or an increase of 106.7% compared to 2010 which was around US$ 108.4 billion. In other words, the average increase in FDI to ASEAN since 2010 is US$ 9.65 billion per year.

Singapore, Indonesia, Vietnam are the prima donna of ASEAN

FDI to ASEAN countries in 2022 will be dominated by Singapore, Vietnam and Indonesia. Interestingly, the three countries have very different economic strengths and structures.

FDI to Singapore is US$ 141.18 billion or around 63% of total FDI to ASEAN in 2022.

This is not without reason considering that Singapore has put all its economic efforts into attracting FDI and creating a suitable trading environment. All his strategies have made Singapore one of the easiest cities in the world to do business.

Singapore also positions itself as a business hub in the Asian region. One of the attractions for foreign investors in Singapore is favorable loans for foreign investors, tax incentives and exemptions, pro-business laws, and the city’s financial stability.

The main economic activities of Singapore residents are industry and services. Almost the majority of this country’s population works in the industrial sector, both manufacturing and machinery, as well as tourism and financial services.

The main sector of Singapore’s economic activity is the manufacturing industry. This sector includes the electronics industry, chemicals, biomedical sciences, logistics, and transportation engineering.

Quoted from the Guide Me in Singapore website , the main economic activities of Singapore residents are industry and services. Almost the majority of this country’s population works in the industrial sector, both manufacturing and machinery, as well as tourism and financial services.

The main sector of Singapore’s economic activity is the manufacturing industry. This sector includes the electronics industry, chemicals, biomedical sciences, logistics, and transportation engineering.

The value of Singapore’s trade in goods and services is equivalent to 185% of Gross Domestic Product (GDP), based on data from the World Bank .

Singapore’s goods exports reached SG$ 969.1 billion in 2020, down from SG$ 1.022 billion in 2019. From the production side, the services sector plays a role of around 75% in the economy, including export-related services.

Vietnam has become another target for foreign investors. Vietnam has become a destination country for foreign investment because the government has the authority to direct foreign investment (PMA) to sectors that support exports. As a result, the FDI contribution to Vietnam is more than 70%.

Apart from that, maintained political and macroeconomic stability and successful growth of around 5-7% each year has kept inflation under control and the business environment is friendly for PMA and even very large tax incentives for PMA have become an attraction for investors.

Vietnam is one of the countries that managed to enter the top 20 foreign investment destinations in 2020. From 1986 until before Covid-19, the total foreign investment (PMA) projects in Vietnam almost reached 27 thousand with registered PMA of US$ 334 billion.

Meanwhile, Vietnam’s foreign direct investment (FDI) in 2022 will reach US$ 14.9 million. In 2019, Vietnam’s FDI also set a record high, reaching US$ 19.9 million.

Vietnam’s success in attracting foreign investment cannot be separated from government policies. There are several reasons why Vietnam has succeeded in becoming a ‘paradise’ country for foreign investment in the world.

First , Vietnam really maintains and pays attention to socio-political stability. The government’s success in maintaining stability is what makes Vietnam’s economic growth continue to grow at around 7% every year.

Second , Vietnam has a lot of free trade cooperation with countries in the region or outside the region.

Apart from being part of the Asean Free Trade Area (AFTA) and the World Trade Organization, Vietnam also has a bilateral trade agreement with the US and a free trade agreement with the European Union which makes investors increasingly interested in investing in Vietnam.

Third , Vietnam also continues to update by changing or adapting legal regulations that increasingly guarantee and benefit foreign investors as a manifestation of the government’s commitment to protecting the interests of foreign investors.

Fourth , the Vietnamese government has a framework that is used as a step to continue to revitalize and improve the business climate. This framework is called the “three breakthroughs”, namely placing market economic institutions and a strong legal framework as controllers; building advanced and integrated infrastructure to facilitate business activities, especially in terms of transportation; and improving the quality of the workforce.

Indonesia itself is also a very attractive country because it has the advantage of very high public consumption and a population dominated by the younger generation and a growing middle class. Apart from that, Indonesia is also rich in various commodities. Furthermore, strong economic policies are also a concern for investors.

Indonesia’s FDI realization continues to increase and even outperforms Domestic Investment (PMDN).

The realization of foreign investors has also shifted both in terms of sector and region. If previously raw mining dominated, downstream mining has now become the new prima donna in Indonesia.

Regions outside Java such as Sulawesi and Maluku have also now become targets for foreign investors in Indonesia.

Which Sectors Are the Most Attractive in ASEAN?

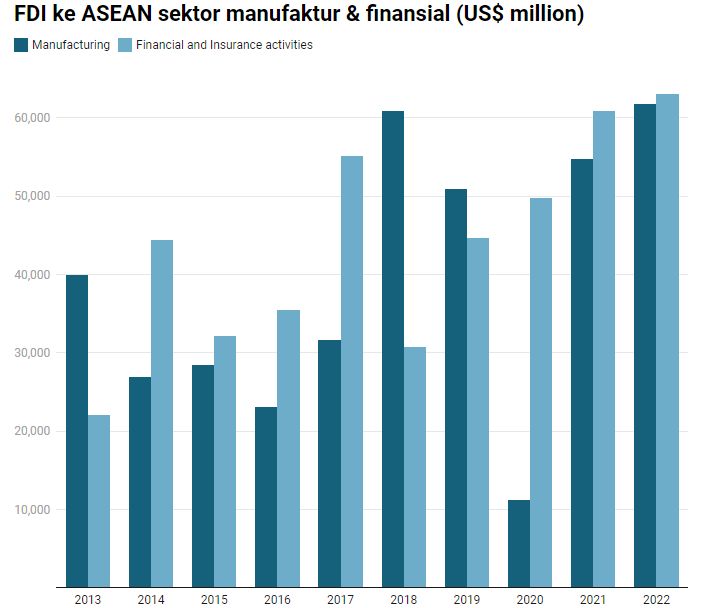

For information, if we look at the industrial sector, around 28% of FDI to ASEAN in 2022 will be intended for financial and insurance activities. Meanwhile, the second position with around 27% of FDI to ASEAN is aimed at the manufacturing industry.

These two sectors are very popular with investors in placing their funds because they are considered quite promising. This investor interest can be seen from the significant growth compared to 2013.

The financial and insurance activity sector in 2013 was recorded at US$ 22.08 billion, while in 2022 it will increase by 185% to US$ 63.07 billion. Or in other words, the increase in FDI into the financial and insurance activity sector has increased by an average of 20%.

Photo: aseanstats.orgFDI to ASEAN Infrastructure and Financial Sectors Photo: aseanstats.orgFDI to ASEAN Infrastructure and Financial Sectors |

Therefore, with the same assumptions, it can be estimated that FDI to ASEAN in this sector has the potential to reach US$ 75.68 billion in 2024.

Meanwhile, in the manufacturing sector, it was recorded in 2013 at only US$ 39.90 billion. Meanwhile, in 2022 there will be growth of around 54% and will reach US$ 61.75 billion.

On average, FDI into this sector has increased by 6% every year. In the same way, it can be assumed that the estimated FDI to ASEAN in this sector is US$ 65.46 billion in 2024.

China, King of Foreign Investors in ASEAN

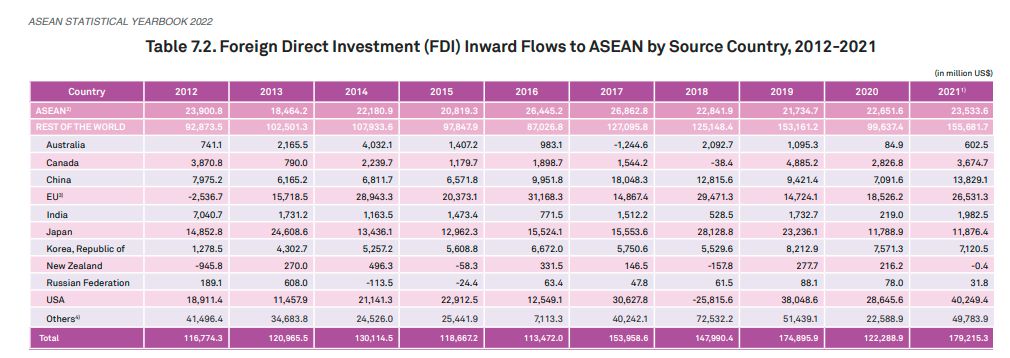

The United States, the European Union and China are the three largest foreign investors in the ASEAN region.

The largest global investor is still the United States with a value of US$ 37 billion or an increase of 6% from the previous year.

The second position is the European Union with a value of US$ 26.53 billion, followed by China (US$ 13.83 billion).

However, if you look at the 2019-2021 data, China recorded the largest increase, namely 96%, while US investment in ASEAN only increased by around 6% and the European Union shot up 80%.

Photo: ASEAN Statistical Book 2022ASEAN Investor Countries Photo: ASEAN Statistical Book 2022ASEAN Investor Countries |

China is a country that is receiving attention considering that the Dragon is the country with the largest economy in Asia and second in the world after the United States (US).

It is known that China’s FDI to ASEAN in 2022 was recorded at US$ 15.39 billion or an increase of around 150% compared to 2013 which was valued at US$ 6.16 billion with the manufacturing sector being the most popular sector since 2019. In 2022, the manufacturing sector is recorded as a portion the largest, namely 33% of China’s total FDI to ASEAN.

However, with the economic slowdown in China, Chinese FDI to ASEAN has the potential to decline. This is beginning to be reflected in the decline in China’s FDI in 2022 when compared to 2021. In 2021, China’s FDI was recorded at US$ 16.6 billion, while in 2022 it was US$ 15.39 billion or a decrease of 7.3%.

In recent months, China’s economic condition has remained in a sluggish condition. The World Bank maintained its forecast for China’s economic growth in 2023 at 5.0%, but lowered its forecast for 2024 to 4.2%.

Even though it is sluggish, the Chinese government has carried out various stimuli to stimulate its economy, such as stimulus to increase demand for the property sector which contracted due to the Evergrande scandal.

Most recently, on Friday (15/9/2023) the People’s Bank of China (PBoC) or China’s central bank will intensify stimulus again by cutting the number of banking reserve ratios or Reserve Requirement Ratio (RRR) for the second time this year.

The stimulus present in China has improved China’s economy, even in the second quarter of 2023, China’s Gross Domestic Product (GDP) grew 6.36% yoy, showing faster growth compared to the 4.5% recorded in the first quarter.

Meanwhile, in the first semester of 2023, China’s economy grew 5.5%. This figure is above China’s GDP target of 5% for this year. With China’s GDP increasing, this will be a positive sentiment for the Chinese economy and can have a good impact on the economy in ASEAN.

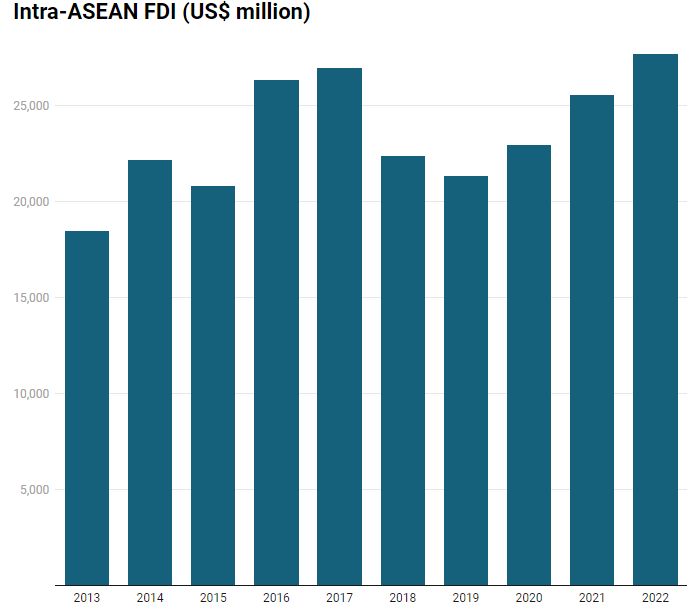

Intra ASEAN or investment between fellow ASEAN members has increased since 2013 from only US$ 18.46 billion to US$ 27.68 billion in 2022. This position is the highest in at least the last 10 years.

The share of foreign investment among ASEAN members has decreased compared to total FDI to ASEAN. In 2021 and 2022, the share of intra-ASEAN FDI will only be around 12%. This is different from 2020 which touched around 19%. This is because external FDI has increased, especially from the US.

The main drivers of FDI growth in ASEAN last year were investments in manufacturing, finance, wholesale and retail trade, transportation and storage, and information and communications.

In total, these five sectors accounted for 86% of the total FDI inflow in ASEAN.

Photo: aseanstats.orgIntra ASEAN FDI Photo: aseanstats.orgIntra ASEAN FDI |

Activities that are carried out and need to be implemented to increase FDI and intra-ASEAN investment, namely by increasing the size and number of start-up companies and unicorns in ASEAN.

Reporting from the 2022 Asean Investment Report, start-ups and unicorns have the nature of growing rapidly with business ideas, innovating and disrupting the market.

Their advantage of being able to raise funds and the drive to grow has led many to regionalize through a number of modalities, such as direct investment in neighboring countries, cross-border mergers and acquisitions, acquisition of strategic shares in other start-ups, establishment of venture capital funds. and partnerships with start-ups and other multinational companies to expand horizontally and vertically in the region.

Reporting from aseanenergy.org , ASEAN electricity demand increased by an average of 6.3% between 2008 and 2018 due to rapid economic growth and urbanization.

To meet these needs, various countries depend on fossil fuels. In 2020, it was recorded that fossil fuels contributed around 78% of electricity generation in ASEAN, with coal accounting for 44%, natural gas 32% and oil 2%. Meanwhile, hydroelectric power plants contributed 16% and other renewable energy only 6%.

Along with world efforts to reduce carbon emissions, ASEAN is also making similar efforts. One way is to increase the portion of NRE in energy use.

The ASEAN Plan of Action for Energy Cooperation (APAEC) outlines an ambitious target of a 23% share of renewable energy (RE) in Total Primary Energy Supply (TPES) and a 35% EBT share of the region’s installed electricity generation capacity by 2025. Due to the deadline As the time approaches, ASEAN member countries (AMS) need to implement bold steps to ensure the achievement of these targets.

Referring to the journal written by Vakulchuk, Overland, and Suryadi in Energy, Ecology, and Environment, it is stated that to achieve the target of 23% renewable energy by 2025, ASEAN needs to get an investment of US$ 27 billion in the field of renewable energy generation and infrastructure every year from 2016 to 2025 or a total of around US$ 290 billion.

For information, the United Nations Conference on Trade and Development (UNCTAD) recorded that international project financing agreements announced in ASEAN increased in value by 73%, from US$ 66.1 billion in 2020 to US$ 114.4 billion, with the largest increase in renewable energy investment and second followed by industrial areas.

However, the realization of renewable energy financing is still relatively low.

In 2020, renewable energy project financing was recorded at only US$ 17.4 billion. Meanwhile, in 2021 there will be a significant increase to US$ 46.5 billion. Meanwhile, financing for industrial area projects in 2020 amounted to US$ 13 billion and in 2021 it was recorded to have increased to US$ 39.2 billion.

These two industries accounted for 75% of international project funding activities in 2021.

Even though renewable energy is something that needs to be increased from year to year, it is important to realize that fossil energy still has an important role, especially oil and natural gas.

The oil and gas industry provides reliable and affordable energy supplies, ensuring economic growth that supports the gradual transition to a net-zero world.

Oil and gas, especially in the ASEAN region, still dominates the energy mix and contributed 56% in 2020 to total primary energy supply (TPES). This figure will increase to 66% in 2050 due to population growth in the baseline scenario.

It must be recognized that the use of oil and gas is important to support regional economic growth, and decarbonization of the oil and gas industry is necessary to limit the dangerous impact of greenhouse gas emissions on the environment.

ASEAN is the most extraordinary market for developing the digital economy. This is because the total population of ASEAN has reached more than 640 million and internet usage will reach 460 million people by 2022. With massive economic growth, ASEAN can become the epicenter and place it in an important position.

ASEAN shows impressive development in the digital era. World digital trade is estimated to reach US$ 10 trillion in 2030, of which US $ 1 trillion, while ASEAN contributes around 10% to global digital trade. In 2020, approximately 80% of internet users in ASEAN engaged in online shopping (Ing and Markus, 2023).

In 2022, the digital economy in ASEAN will reach US$ 194 billion. Meanwhile, the digital economy in ASEAN is projected to increase to around US$ 330 billion in 2025, supported by the implementation of the ASEAN Digital Economy Framework Agreement (DEFA) in 2025 with Malaysia as Chair of ASEAN.

Investments in the digital economy and Industry 4.0 related activities continued to receive strong attention from investors in 2021. FDI in Industry 4.0 related activities in the region is increasing and is expected to continue to grow over the next decade. For example, foreign investment in information and communications increased more than fourfold, to US$ 7 billion, in 2021.

ASEAN is increasingly becoming a start-up hub. The region is witnessing rapid growth in the number of start-ups across an increasingly wide range of business activities, from e-commerce and fintech to travel and hospitality.

The number of start-ups in ASEAN that have raised more than US$1 million in funding almost tripled between 2015 and 2021, from 652 to 1,920.

The growth is much faster than in India (+110%), Europe (+85%) and the United States (+65%). Three member states (Singapore, Indonesia and Malaysia, in that order) account for 83 percent of startups that have raised more than $1 million in the region. However, other ASEAN member countries are also experiencing rapid growth (e.g. Vietnam, the Philippines, and Thailand).

The rapid growth of start-ups is also directly proportional to unicorns. In ASEAN itself, unicorns are growing productively and are only behind the United States, China and India.

The number of unicorns in ASEAN has increased rapidly in recent years, from just 2 in 2014 to 10 in 2018, and then to 46 in 2021.

With the development of the digital economy, the region could register more unicorns in the next few years, depending on financial market conditions.

Most unicorns in ASEAN (38 out of 46) are active in cross-border investments in several countries in the region and beyond. Around 28 unicorns have been established conducting overseas operations through foreign investment, 16 companies have been involved in cross-border Mergers & Acquisitions (M&A), and 33 companies have been involved in establishing joint ventures, strategic partnerships or collaborations with multinational companies or foreign start-ups.

Unicorns in the region acquire strategic assets (technology) to complement existing businesses or diversify into new business areas.

Not only start-ups, the financial sector also receives attention from investors. Banking and finance remains the largest service industry for intraregional investment due to the regional expansion of ASEAN banks and continued investment interest in fintech development.

United Overseas Bank (Singapore) announced plans to invest US$ 500 million over the next five years to scale up its digital banking operations in ASEAN (including Singapore). Siam Commercial Bank (Thailand) expands its activities in Myanmar and Vietnam to offer more digital products and services in host countries. Kasikorn Bank (Thailand) opened a branch in Vietnam and diversified its services in Laos.

Many ASEAN fintech companies will also continue to expand regionally in 2021. Sea (Singapore), a diversified technology company with a fintech branch, acquired Bank BKE (Indonesia) to expand in Indonesia. ASEAN Fintech Group (Singapore) acquired JazzyPay (Philippines), as part of a strategy to expand fintech applications to other ASEAN markets.

In addition, fintech platform Kredivo (Indonesia) is expanding its online lending business to Vietnam. Qoala (Indonesia), an insuretech company leveraging big data, machine learning, Internet of Things and blockchain technology, expanded to Thailand the same year.

This is what makes foreign direct investment (FDI) in the ASEAN region continue to grow, especially in the financial and insurance sectors. Based on 2021 data, the financial and insurance sector is the sector that receives the highest foreign capital, namely 32.0%. Meanwhile, the manufacturing sector is in second place with 25.8%.

Another sector affected by technological advances in ASEAN is logistics. Logistics accounts for around 5% of ASEAN’s GDP and employment, providing jobs for around 17 million people.

It has a wide range of natural benefits and, combined with government commitment and targeted national policies, it makes a major contribution to the national economy.

Reporting from the Investing in ASEAN 2023 report, technological changes and new ways of doing business also have a negative impact on increasing demand for logistics.

ASEAN is now a fast-growing market hosting more than 360 million smartphone-using consumers and the e-commerce market share has grown in recent years.

The logistics sector is expected to reach a value of US$ 142.5 billion by 2025, according to a study published by Google, Temasek and Bain & Co2. This amount is almost four times higher than in 2019, only US$ 36 billion. The outbreak of Covid-19 has also accelerated and strengthened consumer dependence on e-commerce and created even greater potential opportunities.

Furthermore, ASEAN countries support initiatives such as the ASEAN Smart Logistics Network (ASLN), a platform that aims to promote logistics interconnectivity and integration. This is part of the ASEAN Connectivity Master Plan 2025, which encourages integration between members.

For your information, currently two projects have been launched under ASLN, namely the Vinh Phuc Inland Container Depot Logistics Center (superport) between Singapore and Vietnam & the Phnom Penh Logistics Complex in Cambodia (PPLC).

Managed by Vietnam’s T&T Group and Singapore’s YCH Group, Vinh ICD Phuc Logistics Center has funding of more than US$ 158 million to develop an inland container depot and logistics center. Once completed, it will be one of the largest logistics centers in North Vietnam, connecting 20 industrial areas by rail, road and air, as well as links with Hanoi, Hai Phong International Airport and China’s Yunnan Province.

Meanwhile PPLC will be developed by YCH Group, a Singapore-based integrated logistics and supply chain provider, together with Cambodia-based WorldBridge Group. PPLC is expected to cost US$ 191.5 million and is intended to strengthen Cambodia’s position as a regional logistics hub, as this is key to its long-term goal of becoming a high-income country by 2050.

Tourism Sector in ASEAN

Tourism has always been an important part of ASEAN countries’ income. Before the pandemic, this sector accounted for 14.3% of total income combined GDP and provided more than 13% of employment or around 30 million jobs.

From 2000 to 2019, total visitors to ASEAN from various countries in the world continued to grow and in 2019 reached a peak of 143.5 million people with the dominance coming from China (32.28 million) and the main destination was Thailand with a total of 39 visitors. 9 million people. Meanwhile, Indonesia itself only has 16.1 million people.

When Covid-19 hit, the number of international tourists plunged by more than 80% and tourism revenues fell by more than 75%. The initial response to the reduced number of visitors was to increase the number of domestic tourism visitors using discounted prices, subsidized accommodation and increased domestic flights.

Vietnam launched ‘Vietnamese people travel in Vietnam’ while Thailand launched the Rao Tiew Duay Gun Program (‘We travel together’), with a budget of US$ 608 million to help increase domestic tourism.

Post-pandemic, each country has its own program to improve the tourism sector. Thailand, for example, aims to target the premium market. The Thai government launched a long-term residency program to attract foreigners to the country through new visas valid for up to 10 years, tax and investment incentives, easing restrictions on foreign ownership of residential property, and more.

The country’s ambition is to welcome more than one million additional visitors and generate more than US$26 billion in domestic spending over five years, starting in 2022.

Malaysia also launched a comprehensive support program as part of its efforts to improve the tourism industry, including financial assistance and vouchers.

For the record, tourism is very important for the economy of this country, because more than 23% of the population’s jobs are related to this sector. The National Tourism Policy (DPN) 2020-2030 highlights the environment and ecotourism as key opportunities.

The aim of the 10-year plan is to make the country’s tourism companies more competitive, while encouraging sustainability and inclusive sector development and planning for the future.

Apart from these two countries, Laos tourism also needs attention because tourism is the fastest growing industry in the economy and plays an important role in the Laos economy. For information, in the period 1990 to 2015 the number of foreign tourist visits to Laos experienced a continuous increase, with at least 14,400 arrivals recorded in 1990 to 4,684,429 in 2015.

In 2016 this trend changed, when the number of arrivals fell by 10% compared to 2015, and fell further by 8.7% in 2017 (3,868,838 arrivals). However, as a result of efforts to increase arrivals, including prioritizing this sector as a driver of socio-economic development and the success of the Lao PDR visit in 2018, this negative trend began to reverse with a slight increase in arrivals (8.2%) compared to 2017. In 2019 , growth continues with an increase in international arrivals of 14.4% compared to 2018. As a result, the increase in the number of tourists to Laos has had a positive impact on revenues from the tourism sector. In 2012, revenue was recorded at US$506,022,586, while in 2019 it increased by 84% to US$934,710,409.

Reporting from the 2020 Statistical Report on Tourism in Laos, tourism is one of the sectors in the six socio-economic development priorities of the Lao Government program for the 2021-2025 period.

In line with this, the Ministry of Information, Culture and Tourism has formed the National Tourism Development Plan 2021-2025 which focuses on developing, promoting and managing natural, cultural and historical tourism in a green and sustainable manner, tourism integration, as well as contributing to lifting people out of poverty is in line with government policy.

Source : CNBC