Initial gains in Wall Street last Friday failed to find much follow-through, with the DJIA eking out a slight gain (+0.3%) while the S&P 500 (-0.1%) and Nasdaq (-0.2%) closed in the red. The US consumer sentiment index last Friday has smashed past expectations to turn in its highest level since September 2021 (72.6 versus 65.6 consensus), with the stellar read essentially pushing back against recessionary concerns, given that past recessions since 1968 were marked by a decline in the US consumer sentiment data.

That said, earnings results from major US banks were more mixed, with JP Morgan and Wells Fargo beating estimates while Citigroup disappoints. The financial sector ended the day lower by 0.7%, with the Financial Select Sector SPDR Fund having formed a bearish engulfing candle on its daily chart, which could indicate some exhaustion in the sector’s recent rally.

Into the new trading week, the lighter US economic calendar and the Fed blackout period will continue to leave much of the focus on the US earnings season. While estimates suggest that we are currently still in an “earnings recession” with the third consecutive quarter of earnings contraction expected for the S&P 500 in Q2, the divergence in stock market performance (S&P 500 at its highest level since April 2022) seems to be pricing for a bottoming-out in earnings, with a recovery underway in Q3 onwards. Financial updates in the likes of Bank of America, Goldman Sachs, Netflix and Tesla will be key to watch this week to provide any validation.

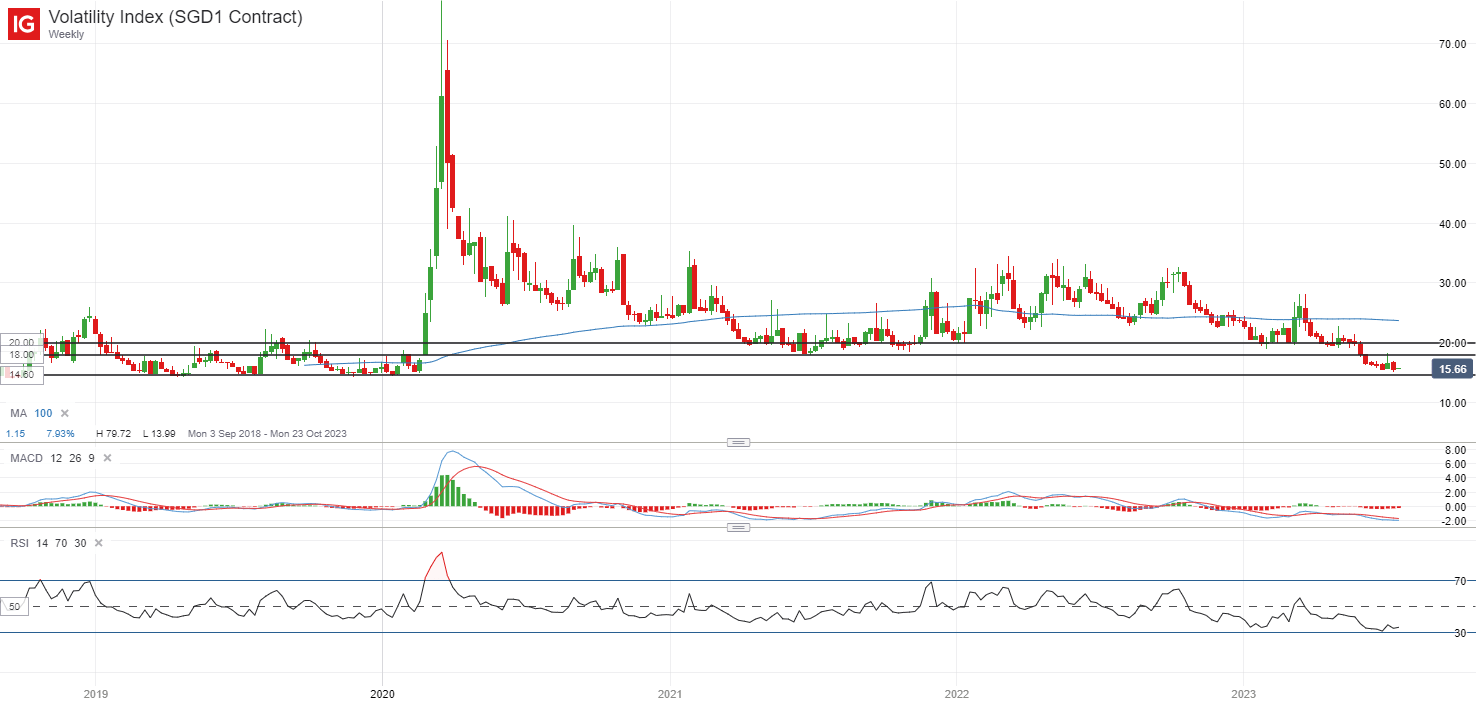

US Treasury yields rebounded last Friday, but the US 10-year yields remain held below a key resistance at the 3.85% level. US interest rate expectations from the Fed funds futures were largely unswayed, with one last 25 basis-point (bp) from the Fed this month still the consensus. The VIX is back to retest its June 2023 low, indicating the broader bullish sentiments despite the near-term risks of a retracement. Further downside will likely leave the 14.60 level as a key support to watch, having held up the index on at least four previous occasions since 2019. On the upside, immediate resistance on watch will be at the 18.00 level.

Source: IG charts

Asia Open

Asian stocks look set for a subdued open, with ASX -0.10% and KOSPI -0.43% at the time of writing. Japan markets will be offline due to Marine Day, while the morning trading session for the Hong Kong markets has been delayed due to the issuance of Typhoon Signal No. 8, potentially setting a quieter tone for markets this morning.

Nevertheless, all eyes will be on a series of China’s economic data releases later including its 2Q GDP, with any weaker-than-expected read likely to serve as a dampener for the broader risk environment. Current expectations are for China’s 2Q GDP growth rate to turn in a 7.3% growth year-on-year, up from the 4.5% in 1Q, but large base effects from last year could mask the underlying dynamics to some extent. Quarter-on-quarter, a 0.5% growth is the consensus.

A series of key economic data will be released alongside as well, such as retail sales (est 3.2% versus 12.7% in June), industrial production (est 2.6% versus 3.5% in June) and fixed asset investment (3.5% versus 4% in June). Overall, an expected moderation in growth across the indicators may continue to point to a more tepid growth outlook for the world’s second largest economy.

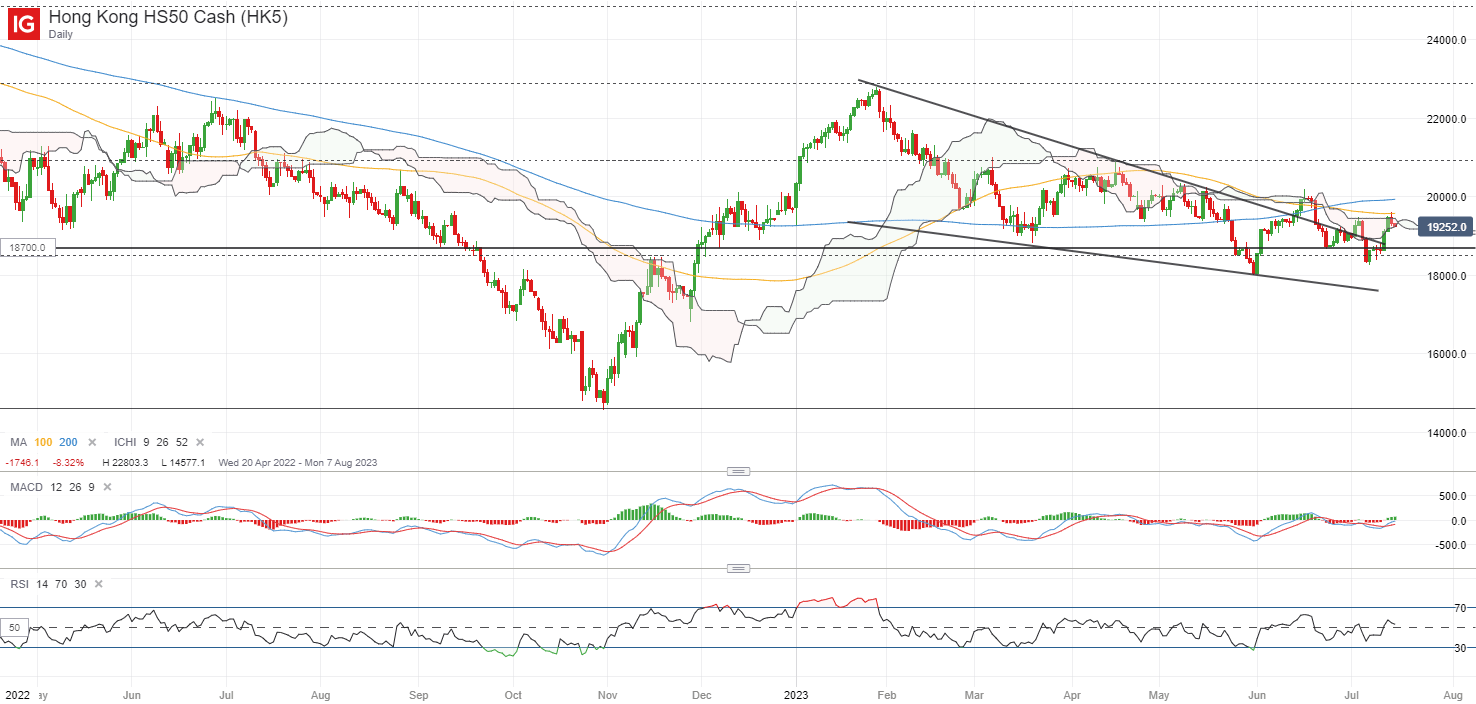

The Hang Seng Index is back to retest the upper edge of its Ichimoku cloud (daily) at the 19,600 level to end last week, with past five interactions since April this year failing to find a successful breakthrough. Near-term, the 19,600 level also coincides with its 100-day moving average (MA). While a bullish crossover on moving average convergence/divergence (MACD) and Relative Strength Index (RSI) above 50 may point to some building upward momentum lately, much is still dependent on a reclaim of its 100-day MA, along with its key psychological 20,000 level.

Source: IG charts

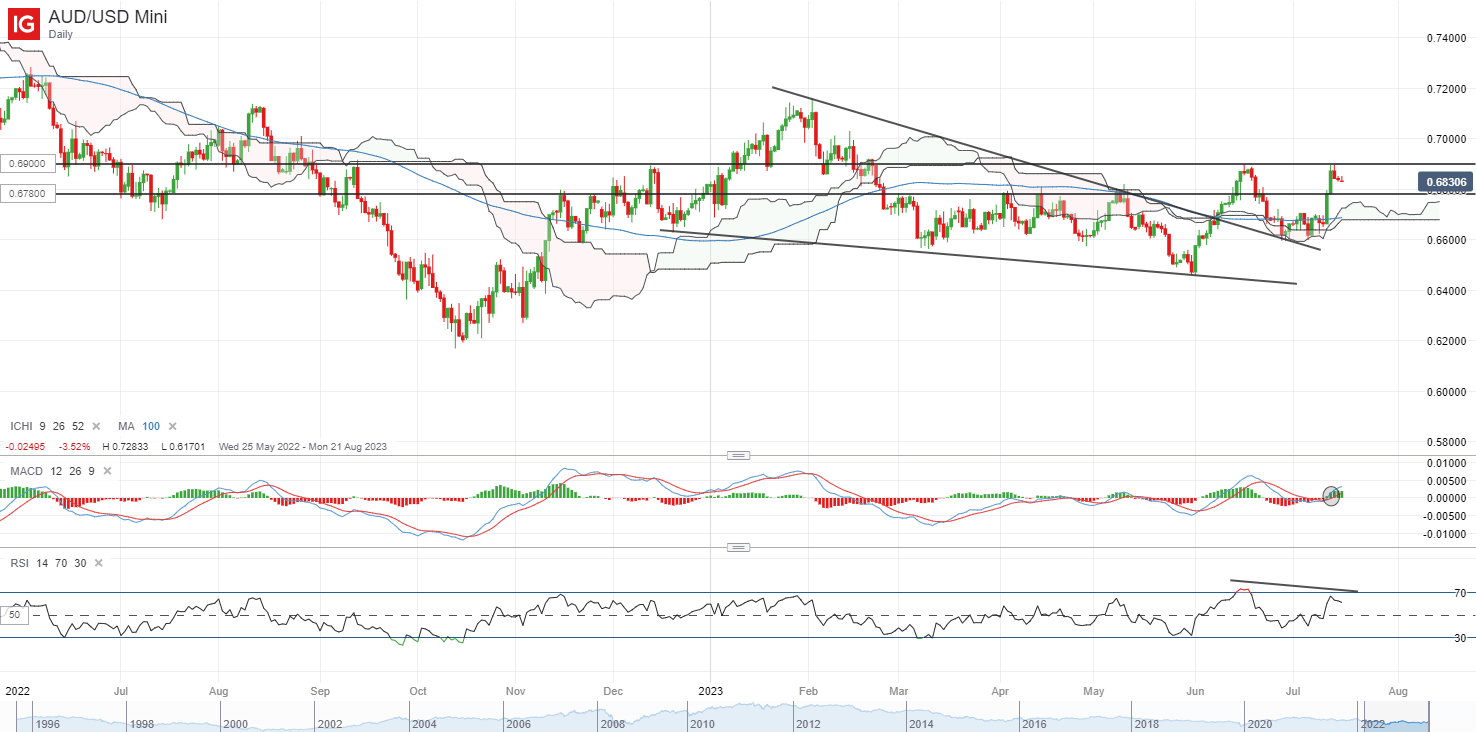

On the watchlist: AUD/USD retesting June 2023 high ahead of China’s data, RBA minutes

The AUD/USD has been taking the recent announcement of Australia’s next Reserve Bank governor, Michele Bullock, in stride as the new appointment largely pointed towards a no-change in monetary policies. But as a series of China’s economic data looms, along with the release of the Reserve Bank of Australia (RBA) minutes tomorrow, the pair is finding some resistance around its 0.690 level with a near-term bearish divergence on its RSI.

On the weekly chart, the 0.690 level also marked the upper edge of its Ichimoku cloud resistance, where the pair has failed to overcome on the past three interactions since March 2022. Ahead, any weaker-than-expected economic data out of China could further translate to some selling pressure. Any downside may leave the 0.678 level on watch as a previous resistance-turned-support. Failure to defend the 0.678 level may potentially prompt a move back towards the 0.660 level, where its previous consolidation lies.

Source : Daily Fx